Some options strategies rely on predicting market direction. The iron condor takes a different approach. It is designed for situations where the underlying asset is expected to remain within a defined price range over a specific period.

The strategy combines two credit spreads: a bull put spread below the current price and a bear call spread above it. Together, they create a range where the trader collects a premium if the underlying stays between the two short strikes. Protective long options on both sides cap the maximum loss.

Iron condors are commonly used on liquid index options such as Nifty, Bank Nifty, and Sensex, where tight spreads and strong liquidity support efficient multi-leg execution. Traders typically deploy them during sideways markets or periods of moderate volatility, when large directional moves are less likely.

#What Is the Iron Condor Strategy?

An iron condor consists of four options with the same expiration but different strikes:

- #Sell one OTM put

Generates premium, defines the lower bound of the target range - #Buy one further OTM put (lower strike)

Caps downside risk, forming the bull put spread - #Sell one OTM call

Generates premium, defines the upper bound of the target range - #Buy one further OTM call (higher strike)

Caps upside risk, forming the bear call spread

The position is established for a net credit; premiums received from the short options exceed premiums paid for the long options. Maximum profit occurs if all four options expire worthless, meaning the underlying stays between the two short strikes at expiration.

The iron condor is a defined-risk version of a short strangle. The long wings cap losses on both sides, reducing margin requirements and psychological exposure compared with naked option selling.

#Short vs long iron condor:

- The standard (short) iron condor is a credit strategy that profits from low movement and IV (Implied Volatility) contraction.

- A long iron condor reverses the structure and profits from large moves, it is not relevant for a low-volatility positioning angle.

#When to Use the Iron Condor Strategy

The iron condor fits specific market conditions:

- #Neutral to mildly directional outlook

The trader expects the underlying to stay within a range or drift slowly without sharp breakouts. - #Range-bound or consolidating markets

After a strong move, many instruments consolidate in horizontal channels. Iron condors monetise these sideways phases. - #Stable or declining implied volatility

The position benefits when IV contracts after entry, reducing option prices and enabling profit-taking before expiration. - #Income generation

Traders use recurring iron condors (weekly or monthly) to systematically harvest time premium in otherwise quiet markets.

#A Nuance on Volatility

Many sources describe iron condors as ideal for "low IV" environments, but systematic studies show better raw performance when trades are opened during elevated implied volatility, premiums are richer, and break-even ranges are wider.

The key is that implied volatility should be high relative to recent history (high IV rank) while the forward view is for volatility to compress and price to stay contained.

Avoid entering iron condors just before known binary events (earnings, RBI policy meetings, budget announcements) that can trigger volatility spikes and directional gaps.

#How the Iron Condor Strategy Works?

#Payoff Structure

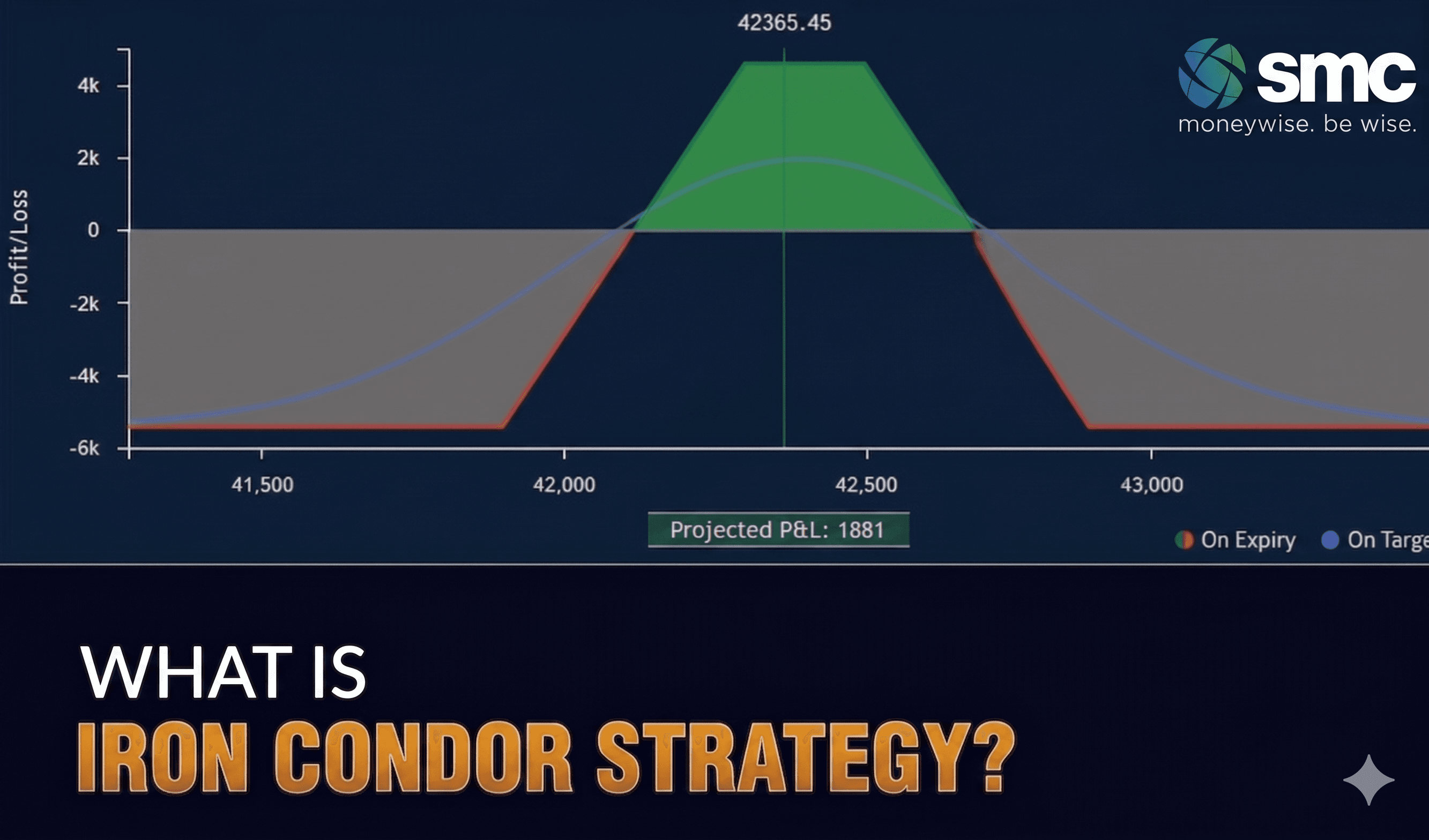

The payoff diagram resembles a flat plateau between the short strikes (the profit zone), with sloping losses beyond the break-even points, capped at the long strikes. The net credit received at entry represents the maximum profit if the underlying stays inside the range.

As time passes, extrinsic value of the OTM options decays. If the underlying remains inside the range and implied volatility stays flat or falls, the iron condor's market value declines, allowing the trader to buy it back for less and lock in profit before expiration.

#Greeks Behaviour

#Time to Expiry

Most practitioners recommend opening iron condors around 30-45 days to expiration (DTE), balancing meaningful premium with relatively fast decay. Shorter DTE provides faster theta but more gamma risk. Longer DTE offers more premium but slower decay.

For weekly income strategies, traders use weekly index options (under 10 DTE), accepting more active management in exchange for rapid decay.

#Structure of an Iron Condor Trade

#Strike Selection

On a liquid index trading at a given spot price:

- Short strikes are placed where option deltas are between 0.15 and 0.30, giving a relatively low probability of being breached by expiration.

- Wing width (distance between short and long strike on each side) is set based on volatility and account size. Wider spreads increase maximum loss but also increase credit and widen the profit range.

- Many traders align short strikes with technical support and resistance zones, selling the put spread below support and the call spread above resistance, to increase the odds that the price stays within the condor.

#Underlying Selection

Preferred underlyings include #liquid index options (Nifty, Bank Nifty, Sensex) and large-cap stocks with tight bid-ask spreads and deep open interest. Illiquid names with wide spreads and low open interest lead to poor executions and make adjustments harder.

#Profit and Loss Potential in Iron Condor

#Maximum Profit

Maximum profit equals the net credit received at entry. It occurs when the underlying settles between the two short strikes at expiration, so all four options expire worthless.

Common practice is to exit when 50-75% of maximum profit has been realised, rather than holding to expiration. This reduces tail risk late in the trade.

#Maximum Loss and Break-Even Points

Maximum loss is limited and equals the width of the wider vertical spread minus the net credit received. For symmetric condors (same width on both sides), only one spread can finish in the money at expiration.

Break-even points at expiration:

- #Lower break-even = short put strike minus net credit per share

- #Upper break-even = short call strike plus net credit per share

#Realistic Expectations

Iron condors offer high probability but small, capped profits relative to the capital at risk. The risk-reward ratio typically ranges from 2:1 to 4:1 (max loss to max profit).

Empirical analyses show that wider condors opened when IV is high can deliver better long-run returns than narrow condors opened in calm markets, at the cost of more pronounced drawdowns during volatility spikes.

#Ideal Market Conditions for Iron Condor

#Price Action

- Range-bound, sideways markets where the underlying oscillates within a band and lacks a strong trend.

- Post-move consolidation inside well-defined support and resistance.

- Not trending or breakout markets, if the underlying is in a strong trend, one side of the condor comes under pressure quickly.

#Volatility Profile

For a "low volatility markets" context, the nuance matters:

- Iron condors benefit from low realised volatility while the trade is open, the underlying does not move aggressively.

- At entry, moderate to elevated implied volatility (roughly 20-35% IV, or VIX in mid-teens to mid-20s) is the sweet spot. Premiums are attractive, but the risk of extreme moves is manageable.

- Extremely low IV reduces credit and narrows break-even ranges, making risk/reward unattractive after transaction costs.

- Extremely high IV (VIX above ~30-35) expands expected price ranges and increases breakout probability. Size down, widen wings, or wait for normalisation.

#Event Calendar

Avoid entering condors just before earnings, central bank meetings, or known macro releases. Favour periods with a relatively light calendar and subdued recent realised volatility.

#Risk Management in Iron Condor Strategy

#Position Sizing

Limit risk per trade to 3-5% of total portfolio equity, especially as a beginner. This controls drawdowns if multiple trades lose consecutively.

Iron condor margins are substantially lower than for naked short strangles due to the protective long legs; some Indian brokers report margin reductions of up to 80% compared with unhedged positions.

Diversify by using multiple smaller condors across different underlying or staggering entry dates to avoid concentrated event risk.

#Trade Management Rules

- #Profit target: Close when 50-75% of the max profit is achieved.

- #Loss limit: Close or adjust at 1.5-2 times the initial credit, or at roughly 60-75% of maximum loss.

- #Time-based exit: Consider closing 5-7 days before expiration to avoid rapid gamma acceleration and assignment risk.

#Volatility and Assignment Risk

Sudden IV spikes can increase mark-to-market losses even if the price has not breached short strikes; monitor IV alongside price. Early assignment risk (for American-style options) rises near ex-dividend dates or deep in-the-money situations; exiting or rolling threatened legs mitigates this.

#Process Over Discretion

Maintain a written plan covering strike selection criteria, IV entry thresholds, profit/loss exit triggers, and adjustment rules. Over-leverage, excessively narrow wings, and trading condors in clearly trending markets are the most common mistakes.

#Adjustments and Exit Strategies

#When to Adjust

Adjustments are triggered when the price approaches or breaches a short strike, or when unrealised loss hits a predefined threshold. The goal is to reduce max loss, collect additional credit, or re-centre the profit zone, while recognising that adjustments often lower the probability of profit.

#Common Adjustment Techniques

#Roll the unchallenged side closer:

Close the profitable (untested) spread and reopen it closer to current price. Collects additional credit and widens break-evens, but narrows the profitable range.

#Roll the entire condor to a later expiration:

Close all four legs and reopen at a later date, ideally for a net credit. Extends the time for price to return to a profitable range.

#Add a directional hedge:

Add a debit spread or long option on the threatened side to offset further adverse moves. Costs some of the initial credit but reduces downside if the move continues.

#Convert to a butterfly or narrower variation:

Roll one side to create an iron butterfly, reducing maximum loss but concentrating risk closer to the money.

#Full exit at predefined loss:

Many systematic traders prefer mechanical exits over complex adjustments. Simpler to execute, avoids increasing exposure in a losing trade, and is preferable for newer traders building experience.

#Adjusting vs Exiting

Adjustments can smooth P&L and avoid full max loss, but they add complexity, extra commissions, and can turn a losing trade into a larger, longer, more complicated position. For beginners, straightforward stop-loss exits are usually the better default.

#Advantages and Limitations of Iron Condor Strategy

#Advantages

#Defined risk and reward:

Both maximum profit and loss are known at entry, enabling precise position sizing.

#High-probability income:

Works well when markets are directionless; can generate consistent premium income through repeated deployments.

#Benefits from time decay and IV contraction:

Naturally aligned with the decay of option time value.

#Lower margin than naked strategies:

Hedged wings reduce margin requirements, making the approach accessible to smaller accounts.

#Limitations

#Unfavourable risk-reward ratio:

Max loss is typically 2-4 times max profit. A few large losses can wipe out many small gains if risk management is weak.

#Sensitive to volatility spikes and trends:

Strong directional moves or IV shocks can cause rapid mark-to-market losses, even before the short strike is breached.

#Complexity and monitoring:

Four legs, multiple Greeks, and possible adjustments make iron condors more complex than single-leg strategies. Ongoing monitoring is required.

#Transaction costs:

Four-leg structures incur more commissions and are more exposed to slippage, especially on less liquid underlyings.

Iron condor strategies require disciplined execution and timely decisions. Open a Demat account with SMC to trade efficiently with integrated research, real-time data, and multi-segment access.